Introduction: The Big Question in Investing

Every investor eventually asks this question:

Can I consistently beat the market?

If markets are inefficient, then skilled investors can identify mispriced stocks and earn superior returns.

But if markets are efficient, then consistently beating the market becomes nearly impossible.

This debate lies at the heart of one of the most influential theories in finance:

The Efficient Market Hypothesis (EMH).

EMH challenges active investing strategies and directly connects to the assumptions behind:

- Modern Portfolio Theory (MPT)

- Capital Asset Pricing Model (CAPM)

In fact, CAPM assumes markets are efficient. So now we examine:

Is that assumption realistic?

In this deep dive, you will learn:

- What EMH really means

- The three forms of market efficiency

- How EMH affects technical and fundamental analysis

- The concept of Random Walk Theory

- Evidence supporting EMH

- Evidence against EMH

- Market anomalies

- The rise of behavioral finance

- Practical implications for investors

Let’s begin from the foundation.

1. What Is the Efficient Market Hypothesis?

The Efficient Market Hypothesis (EMH) states:

Asset prices fully reflect all available information.

In simple terms:

- Prices adjust quickly to new information.

- No investor can consistently achieve abnormal returns using publicly available information.

If markets are efficient:

- Stocks are always fairly priced.

- There are no “cheap” or “overpriced” stocks for long.

- Any mispricing is quickly corrected.

This idea was formally developed by economist Eugene Fama in the 1960s.

EMH does NOT say prices are always correct.

It says:

Prices are the best possible estimate based on available information.

2. Why EMH Matters

EMH affects nearly every investment decision:

- Should you actively pick stocks?

- Should you use technical analysis?

- Should you rely on fundamental analysis?

- Should you invest in index funds?

If EMH is true, passive investing becomes very powerful.

If EMH is false, active investors may outperform.

3. The Three Forms of EMH

EMH exists in three different forms:

- Weak Form

- Semi-Strong Form

- Strong Form

Each form assumes a different level of information efficiency.

3.1 Weak Form Efficiency

Weak-form EMH states:

All past trading information is already reflected in stock prices.

This includes:

- Historical prices

- Trading volumes

- Chart patterns

Implication:

Technical analysis should not consistently generate abnormal profits.

If weak-form efficiency holds:

Looking at past charts cannot help predict future prices.

3.2 Semi-Strong Form Efficiency

Semi-strong EMH states:

All publicly available information is already reflected in stock prices.

This includes:

- Financial statements

- Earnings reports

- News announcements

- Economic data

- Industry reports

Implication:

Neither technical nor fundamental analysis can consistently outperform the market.

When new public information is released, prices adjust almost immediately.

3.3 Strong Form Efficiency

Strong-form EMH states:

All information — public and private — is reflected in stock prices.

This includes:

- Insider information

- Confidential corporate data

Implication:

Not even insiders can consistently earn abnormal returns.

This is the strongest and most controversial form.

4. EMH and Technical Analysis

Technical analysis attempts to:

- Identify patterns in price charts

- Predict future price movements

- Exploit trends and momentum

Under weak-form EMH:

Past price data is already incorporated into current prices.

Therefore:

Technical analysis should not consistently work.

However, short-term momentum strategies sometimes challenge this assumption.

5. EMH and Fundamental Analysis

Fundamental analysis involves:

- Studying financial statements

- Estimating intrinsic value

- Comparing price vs value

Under semi-strong EMH:

Public information is already priced in.

This means:

By the time you analyze a company’s earnings, the market has already adjusted.

Therefore:

Consistently finding undervalued stocks becomes extremely difficult.

6. Random Walk Theory

EMH connects closely with Random Walk Theory.

Random Walk Theory states:

Stock price changes are random and unpredictable.

Each price movement is independent of past movements.

Imagine flipping a coin:

- Each flip is independent.

- Past flips do not influence future flips.

If markets follow a random walk:

Short-term price prediction becomes nearly impossible.

7. Evidence Supporting EMH

Several findings support EMH.

7.1 Rapid Price Adjustments

Stock prices react almost instantly to:

- Earnings announcements

- Economic data releases

- News events

This suggests markets process information quickly.

7.2 Professional Fund Performance

Research shows:

Most actively managed mutual funds fail to consistently outperform index funds over long periods.

After fees and costs, many active managers underperform.

7.3 Difficulty in Consistent Outperformance

While some investors outperform temporarily:

Sustained long-term outperformance is rare.

This supports the idea that beating the market consistently is difficult.

8. Evidence Against EMH

Despite strong support, EMH faces criticism.

8.1 Market Bubbles

Examples:

- Dot-com bubble

- Housing bubble

- Cryptocurrency manias

Prices rose far above fundamental value.

This suggests markets can become irrational.

8.2 Market Crashes

Sharp crashes sometimes appear disconnected from fundamental changes.

This challenges the idea of rational pricing.

8.3 Market Anomalies

Certain patterns seem to contradict EMH.

9. Market Anomalies

Market anomalies are patterns that seem inconsistent with efficiency.

Examples:

9.1 January Effect

Small-cap stocks historically performed better in January.

9.2 Momentum Effect

Stocks that performed well recently tend to continue performing well short term.

9.3 Value Premium

Value stocks often outperform growth stocks over long periods.

These anomalies suggest markets may not be perfectly efficient.

10. Behavioral Finance vs EMH

Behavioral finance challenges EMH by arguing:

Investors are not perfectly rational.

Human biases influence decisions:

- Overconfidence

- Herd behavior

- Loss aversion

- Anchoring

Emotions can drive:

- Bubbles

- Panic selling

- Overreactions

This suggests prices may deviate from fundamental value.

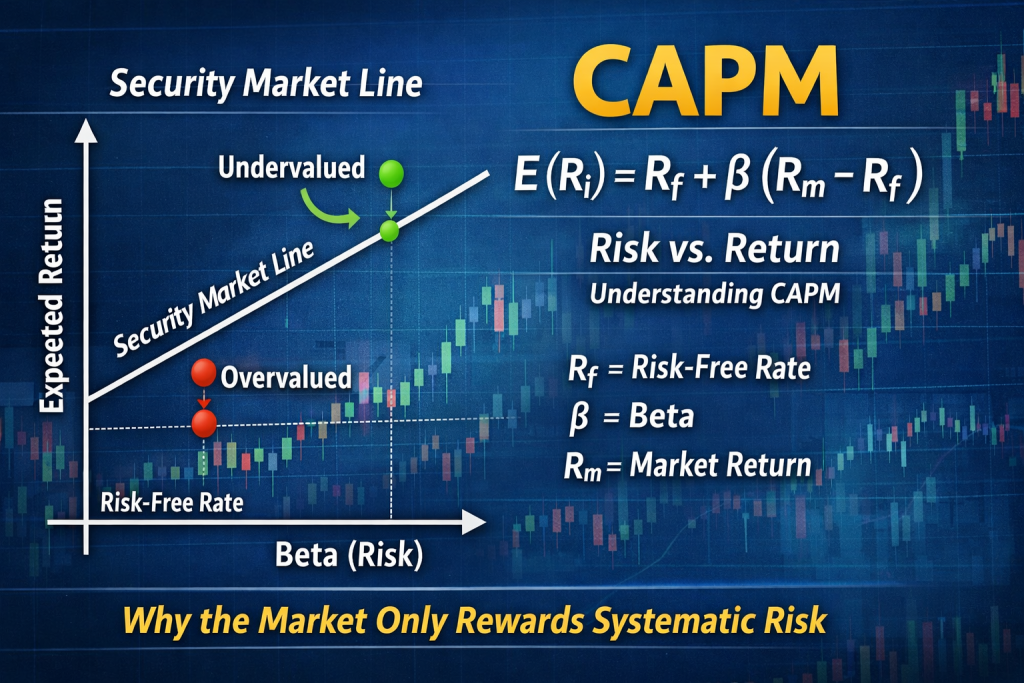

11. EMH and CAPM Connection

CAPM assumes markets are efficient.

If markets are not efficient:

- Beta may not fully explain returns.

- Other risk factors matter.

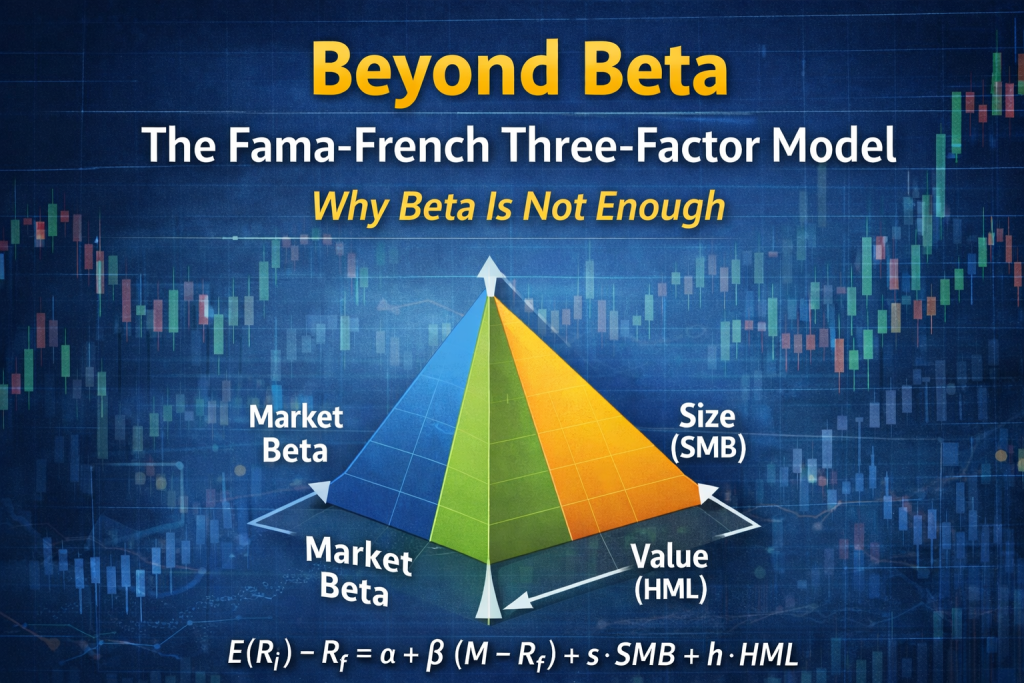

This led to multi-factor models like:

- Fama-French Three-Factor Model

- Arbitrage Pricing Theory (APT)

12. Practical Implications for Investors

Let’s bring this to real-world investing.

12.1 If EMH Is Mostly True

- Passive investing makes sense.

- Low-cost index funds are powerful.

- Reducing fees is critical.

- Long-term investing is key.

12.2 If Markets Are Imperfect

- Opportunities may exist.

- Skill, discipline, and patience matter.

- Behavioral mistakes create temporary mispricing.

However:

Outperformance requires:

- Deep research

- Emotional discipline

- Risk management

13. What Should Retail Investors Do?

From a practical perspective:

For most investors:

- Diversified index funds

- Long-term strategy

- Low fees

- Avoid frequent trading

These principles align with both EMH and real-world evidence.

Trying to time the market consistently is extremely difficult.

14. A Balanced View of EMH

Markets are not perfectly efficient.

But they are highly competitive.

Prices reflect information quickly.

Opportunities exist — but they are rare and difficult to exploit consistently.

EMH is not absolute truth.

It is a powerful framework.

Conclusion: Can You Beat the Market?

The Efficient Market Hypothesis teaches us:

Beating the market consistently is extremely difficult.

Some investors may succeed temporarily.

But long-term, sustainable outperformance is rare.

For most investors:

Discipline, diversification, and low costs outperform aggressive trading.

Understanding EMH helps you:

- Avoid unrealistic expectations

- Reduce emotional decisions

- Focus on long-term wealth building