Introduction: Beyond CAPM

The Capital Asset Pricing Model (CAPM) taught investors an essential lesson:

- Risk (measured by Beta) determines expected return.

- The market compensates investors for systematic risk.

Yet real-world research showed a problem:

- Some stocks consistently outperformed what CAPM predicted.

- Beta alone could not explain differences in returns.

This led to the Fama-French Three-Factor Model, developed by Eugene Fama and Kenneth French in the 1990s.

This model adds two additional factors to Beta:

- Size (SMB – Small Minus Big)

- Value (HML – High Minus Low)

These factors help explain returns that CAPM could not, giving investors a more accurate framework.

In this article, you will learn:

- The problem with CAPM

- What SMB and HML factors are

- The full Fama-French formula

- How this model differs from CAPM

- Practical applications in portfolio management

- Factor investing and ETFs

- Strengths and limitations

- How investors can use this knowledge today

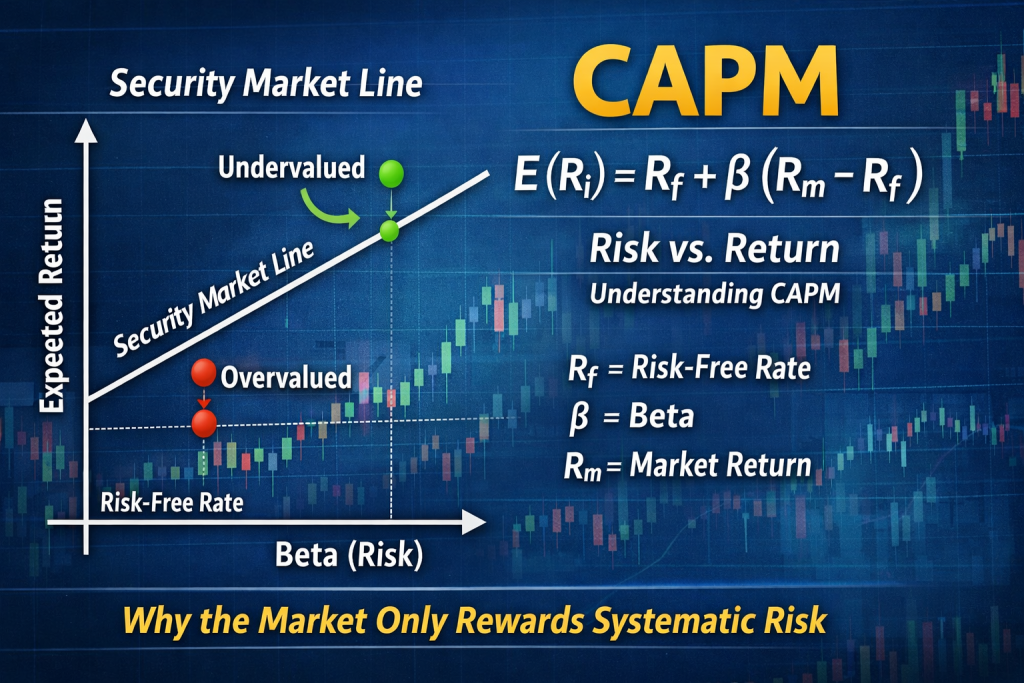

1. The Problem with CAPM

CAPM assumes:

[

E(R_i) = R_f + \beta_i (R_m – R_f)

]

Where Beta captures systematic market risk.

Yet research in the 1970s-80s revealed patterns CAPM couldn’t explain:

- Small-cap outperformance: Smaller companies earned higher returns than Beta predicted.

- Value stock outperformance: Stocks with high book-to-market ratios (value stocks) outperformed growth stocks.

These patterns are called market anomalies, and they challenged the idea that Beta alone explains returns.

2. The Size Effect: SMB (Small Minus Big)

The Size Effect reflects that:

- Small-cap stocks tend to outperform large-cap stocks over long periods.

Fama and French quantified this as:

- SMB (Small Minus Big) = average return of small-cap portfolios − average return of large-cap portfolios

This factor captures the extra return investors earn for holding smaller, riskier companies.

Example:

- Small-cap ETF return = 12%

- Large-cap ETF return = 9%

- SMB factor = 3%

3. The Value Effect: HML (High Minus Low)

The Value Effect reflects that:

- Stocks with high book-to-market ratios (value stocks) outperform low book-to-market (growth) stocks.

HML (High Minus Low) = average return of high book-to-market portfolios − average return of low book-to-market portfolios

This factor captures returns related to undervalued or “cheap” stocks.

Example:

- High B/M portfolio = 14%

- Low B/M portfolio = 10%

- HML factor = 4%

4. The Fama-French Three-Factor Formula

The formula extends CAPM:

[

E(R_i) – R_f = \alpha + \beta_i (R_m – R_f) + s_i \cdot SMB + h_i \cdot HML + \epsilon

]

Where:

- E(Ri) = expected return of stock i

- Rf = risk-free rate

- βi = market Beta (systematic risk)

- s_i = sensitivity to SMB (size factor)

- h_i = sensitivity to HML (value factor)

- ε = residual (unexplained return)

- α = intercept (abnormal return not explained by factors)

Key points:

- β still measures market risk.

- s_i measures how sensitive the stock is to small vs large company returns.

- h_i measures sensitivity to value vs growth returns.

5. Comparison: CAPM vs Fama-French

| Feature | CAPM | Fama-French 3-Factor |

|---|---|---|

| Risk Factors | Beta only | Beta + SMB + HML |

| Explains | Market risk | Market + size + value |

| Predictive Power | Limited for anomalies | Stronger across small & value stocks |

| Use in Practice | Cost of equity, valuation | Factor investing, portfolio tilt |

| Limitations | Ignores other anomalies | Still doesn’t capture momentum, liquidity, behavior |

In short:

- CAPM = simple, foundational

- Fama-French = more accurate and practical for real-world returns

6. Practical Applications in Portfolio Management

6.1 Factor Investing

Investors can tilt portfolios toward:

- Small-cap stocks → higher potential return

- Value stocks → capture HML premium

6.2 ETFs and Index Funds

Many factor-based ETFs replicate Fama-French factors:

- Small-cap value ETFs

- Value-weighted indexes

Investors can gain factor exposure passively.

6.3 Risk Management

Understanding s_i and h_i helps:

- Assess factor exposure

- Diversify beyond market Beta

- Reduce portfolio volatility

7. Real-World Example

Suppose you have a portfolio:

- Beta = 1.1

- s_i = 0.6 (small-cap tilt)

- h_i = 0.8 (value tilt)

Expected excess return:

- Market factor = 8%

- SMB = 3%

- HML = 2%

Contribution:

- Beta contribution = 1.1 × 8% = 8.8%

- SMB contribution = 0.6 × 3% = 1.8%

- HML contribution = 0.8 × 2% = 1.6%

Total expected excess return = 12.2%

This illustrates how factor exposure affects portfolio return beyond CAPM Beta.

8. Strengths of the Fama-French Model

- Explains anomalies CAPM cannot

- Provides a framework for factor investing

- Widely adopted in academic research

- Practical for portfolio construction

9. Limitations

- Does not include momentum (other factors exist)

- Requires detailed portfolio data

- Historical factor premiums may not persist

- Sensitive to market regime changes

10. How It Changed Modern Investing

The Fama-French model:

- Inspired factor-based ETFs

- Influenced portfolio management strategies

- Provided a deeper understanding of systematic risk beyond Beta

It showed:

Investors are rewarded not just for market risk, but also for exposure to size and value factors.

11. Practical Advice for Investors

For retail investors:

- Consider diversified factor ETFs

- Use small-cap and value tilts for long-term potential

- Understand your factor exposure alongside Beta

- Avoid over-concentration or chasing short-term anomalies

- Keep fees low and focus on long-term returns

This balances academic theory with real-world application.