For decades, investors searched for a simple question:

Why do some stocks consistently outperform others?

Traditional finance once suggested that markets were largely efficient and that consistent outperformance was nearly impossible. However, modern financial research has revealed that certain characteristics — known as factors — can help explain why some investments deliver higher returns over time.

This discovery gave rise to factor investing, a systematic approach to building portfolios based on proven drivers of returns.

Instead of trying to guess which individual stocks will succeed, factor investors focus on broad characteristics that historically generate higher returns.

Today, factor investing is widely used by:

- Institutional investors

- Pension funds

- Hedge funds

- Asset managers

- Long-term individual investors

In this article, we’ll explore:

- What factor investing is

- The evolution of asset pricing models

- The most important investment factors

- Why these factors work

- How investors build factor portfolios

- The risks and limitations of factor investing

By the end, you’ll understand why factor investing is considered one of the most powerful frameworks in modern finance.

1. What Is Factor Investing?

Factor investing is an investment strategy that targets specific characteristics — called factors — that are associated with higher long-term returns.

Rather than selecting stocks based purely on intuition or speculation, factor investors build portfolios that emphasize these systematic drivers of performance.

Examples of factors include:

- Value

- Size

- Momentum

- Quality

- Low volatility

Each factor represents a measurable attribute that historically explains differences in stock returns.

For example:

- Value stocks tend to outperform expensive growth stocks over long periods.

- Smaller companies often grow faster than larger ones.

- Stocks with strong recent performance frequently continue performing well in the short term.

By combining these factors in a disciplined way, investors aim to improve returns while managing risk.

2. The Evolution of Asset Pricing Models

To understand factor investing, it’s helpful to look at how financial theory evolved.

Early models attempted to explain stock returns using a single factor — market risk.

One of the most famous models was the

Capital Asset Pricing Model.

CAPM proposed that a stock’s expected return depends on:

- The risk-free rate

- The overall market return

- The stock’s beta (its sensitivity to market movements)

While CAPM was groundbreaking, researchers later discovered that it could not fully explain stock returns.

This led to the development of more advanced models.

One of the most influential was the

Fama–French Three-Factor Model developed by

Eugene Fama and

Kenneth French.

Their research introduced two additional factors:

- Size

- Value

These factors helped explain why certain stocks consistently outperformed the market.

Over time, additional factors such as momentum and quality were added, forming the foundation of modern factor investing.

3. What Is a Factor?

A factor is a characteristic that helps explain differences in investment returns.

To qualify as a reliable factor, it typically must meet several criteria:

- Historical evidence – The factor has shown persistent performance across decades.

- Economic rationale – There is a logical explanation for why the factor should exist.

- Robustness – The factor works across multiple markets and asset classes.

- Investability – Investors can realistically build portfolios around it.

When a factor satisfies these criteria, it becomes a useful tool for systematic investing.

4. The Five Most Important Investment Factors

While many factors have been studied, five have gained widespread acceptance in academic and professional investing.

Value

The value factor focuses on stocks that appear undervalued relative to their fundamentals.

Typical indicators include:

- Low price-to-earnings ratios

- Low price-to-book ratios

- High dividend yields

Value investors believe that markets sometimes overreact to negative news, causing good companies to become temporarily undervalued.

When prices eventually recover, value investors benefit.

Size

The size factor refers to the tendency of smaller companies to outperform larger companies over long periods.

Small companies often offer:

- Higher growth potential

- Greater market inefficiencies

- Less analyst coverage

However, they may also carry higher risk.

Because of this, investors often demand higher expected returns from small-cap stocks.

Momentum

The momentum factor reflects the tendency for assets with strong recent performance to continue performing well in the short term.

Momentum strategies typically involve:

- Buying stocks that have recently outperformed

- Selling or avoiding stocks that have underperformed

Momentum is widely observed across:

- Stocks

- Bonds

- Commodities

- Currencies

This factor is often linked to behavioral biases such as herding and delayed information processing.

Quality

The quality factor focuses on financially strong companies with stable earnings and healthy balance sheets.

Quality companies often demonstrate:

- High profitability

- Low debt levels

- Strong cash flow

- Efficient management

These businesses tend to perform better during economic downturns and provide more stable long-term returns.

Low Volatility

The low volatility factor challenges the traditional belief that higher risk always leads to higher returns.

Research shows that stocks with lower price volatility have sometimes delivered better risk-adjusted returns than highly volatile stocks.

Possible explanations include:

- Behavioral biases

- Institutional constraints

- Investor preference for “lottery-like” high-risk stocks

5. Why Factors Work

Researchers have proposed several explanations for why investment factors persist.

Risk-Based Explanation

Some factors may represent compensation for additional risk.

For example:

- Small companies may be more vulnerable during recessions.

- Value stocks may include companies experiencing financial distress.

Investors demand higher expected returns for holding these risks.

Behavioral Explanation

Human psychology also plays a major role.

Investors often:

- Overreact to negative news

- Follow herd behavior

- Chase recent winners

These biases create pricing inefficiencies that factor strategies can exploit.

Structural Market Inefficiencies

Institutional constraints may also contribute.

For example:

- Many funds are restricted from buying small-cap stocks.

- Some investors avoid unpopular or distressed companies.

These limitations create opportunities for systematic investors.

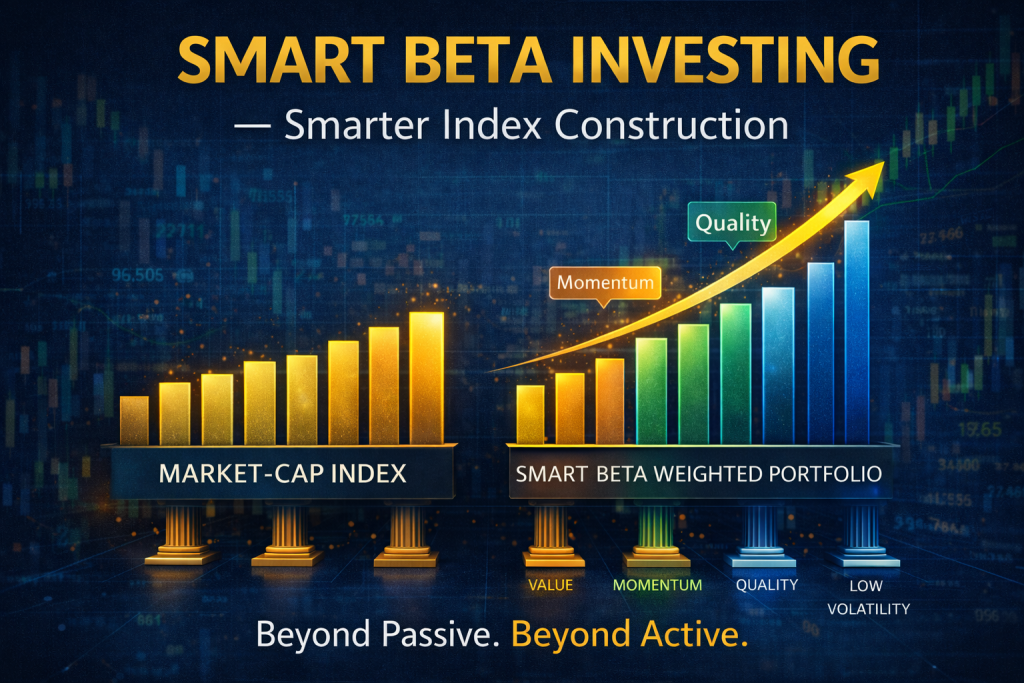

6. Smart Beta Investing

Factor investing is often implemented through smart beta strategies.

Traditional index funds are market-capitalization weighted, meaning larger companies receive greater weight.

Smart beta strategies modify this approach by weighting stocks based on factors such as:

- Value

- Momentum

- Quality

- Low volatility

The goal is to improve returns or reduce risk compared to traditional indexes.

Smart beta has become extremely popular among institutional investors and ETF providers.

7. Multi-Factor Portfolios

Many investors prefer multi-factor portfolios rather than relying on a single factor.

This approach combines several factors to create a more balanced investment strategy.

For example:

- Value + Momentum

- Quality + Low Volatility

- Size + Value + Momentum

Multi-factor portfolios help diversify factor exposure and reduce periods of underperformance.

8. Factor Cycles

Factors do not outperform consistently every year.

Instead, they go through performance cycles.

For example:

- Value may outperform for several years.

- Then momentum or growth strategies may dominate.

These cycles can last for long periods.

Successful factor investors remain disciplined during these fluctuations.

9. How Retail Investors Use Factor Investing

Individual investors can access factor strategies through several methods.

Factor ETFs

Many exchange-traded funds track factor-based indexes.

Examples include ETFs focusing on:

- Value stocks

- Momentum stocks

- Quality companies

Portfolio Tilting

Investors may tilt their portfolios toward specific factors.

For example:

- Increasing exposure to small-cap stocks

- Adding value-oriented funds

Systematic Screening

Investors can also use screening tools to identify companies with strong factor characteristics.

For instance:

- Low valuation ratios

- Strong earnings growth

- High profitability

10. Risks of Factor Investing

Although factor investing is powerful, it is not risk-free.

Important risks include:

Factor Crowding

If too many investors follow the same strategy, returns may decline.

Long Drawdowns

Factors can experience long periods of underperformance.

Investors must maintain patience and discipline.

Overfitting

Some factors appear successful in historical data but fail in real markets.

This happens when researchers accidentally identify patterns that occurred by chance.

Careful validation is essential.

11. Practical Guidelines for Factor Investors

For investors interested in factor investing, several best practices can help improve outcomes.

Diversify across factors

Avoid relying on a single factor.

Use systematic rules

Emotional decision-making often undermines long-term strategies.

Maintain a long-term horizon

Factors may take years to deliver their full benefits.

Control costs

Frequent trading can reduce returns through transaction fees and taxes.

12. The Future of Factor Investing

Factor investing continues to evolve.

Researchers are exploring new factors such as:

- Investment intensity

- Profitability measures

- Environmental, social, and governance (ESG) characteristics

At the same time, advances in technology and data analysis are making systematic strategies more accessible than ever.

As financial markets become more complex, factor investing provides a structured framework for understanding risk and return.

13. Final Thoughts

Factor investing represents one of the most important developments in modern finance.

Instead of relying on speculation or market timing, it focuses on systematic drivers of long-term returns.

By targeting proven characteristics such as:

- Value

- Size

- Momentum

- Quality

- Low volatility

investors can build diversified portfolios designed to capture multiple sources of return.

While no strategy guarantees success, factor investing provides a disciplined, research-based approach to navigating financial markets.

For long-term investors seeking a balance between theory and practice, it remains one of the most powerful frameworks available today.